European alternative protein 2024 investment figures mark return to growth, but show need for better funding options

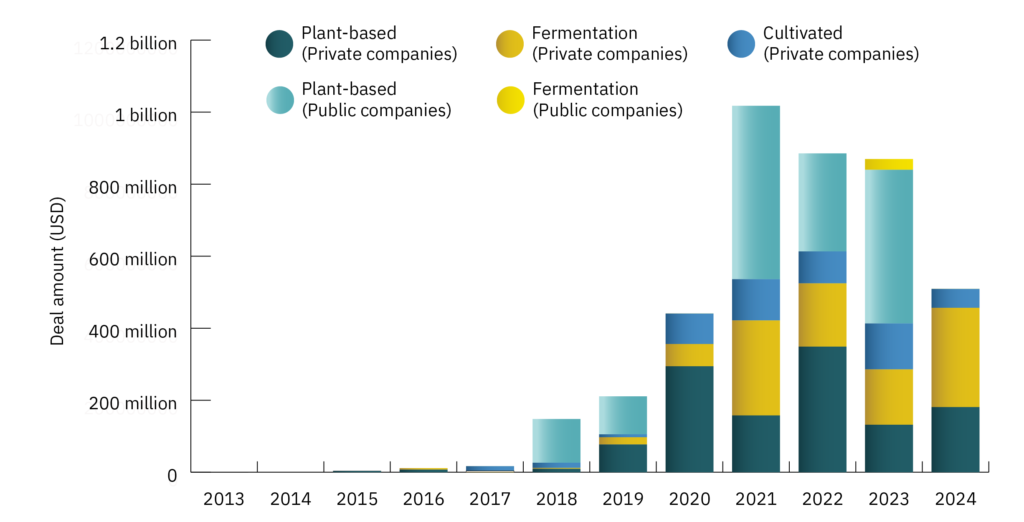

The latest investment figures show European privately held companies developing plant-based foods, cultivated meat, and fermentation raised nearly $509 million (€470 million) in 2024 – a 23% increase from the previous year.

Dieser Artikel ist hier auch auf Deutsch verfügbar. Questo articolo è disponibile anche in italiano.

30 April 2025

The latest investment figures show European privately held companies developing plant-based foods, cultivated meat, and fermentation raised nearly $509 million (€470 million) in 2024 – a 23% increase from the previous year.

In addition to this investment, alternative protein companies brought in $68 million (€63 million) through grants from organisations such as public entities – a 137% increase from the previous year.

This marks a significant trend as governments begin to recognise the role that protein diversification can play in contributing to food security, and as startups begin to shift away from relying on the venture capital that was associated with the sector’s rapid expansion earlier this decade.

To maintain this momentum, alternative protein companies must seek new and innovative funding sources, and governments must ensure these options are available.

In Germany, investments in alternative proteins amounted to $145 million (€134 million) last year. This is by far the largest amount ever invested in this sector in Germany in a single year, five times the figure for the weak year of 2023, and means that German companies accounted for 28% of investments in Europe in 2024.

Fermentation sector on the rise

Net Zero Insights (NZI) figures, analysed by the Good Food Institute (GFI) and included in our latest State Of The Industry reports, reveal that companies developing animal-free foods and ingredients using innovative fermentation techniques continued to attract record investments last year.

Those working on precision fermentation, which uses organisms such as yeast to develop ingredients bringing the familiar flavour and texture of foods like meat, eggs and cheese to plant-based products, raised $130 million (€120 million) from investors in 2024 – more than three times as much as in the previous year.

Europe’s biomass fermentation companies – which use a process similar to beer or yoghurt production to grow large amounts of protein very quickly, such as growing mycoprotein from fungi – raised $129 million (€119 million), a 10% increase.

It’s encouraging to see that many of last year’s largest investments in fermentation, which can help build a circular economy by transforming agricultural byproducts into nutritious food, came from large public funding bodies.

The European Innovation Council (EIC) – established under the EU’s Horizon Europe programme – supported a $58 million (€54 million) funding round enabling Germany’s Infinite Roots to expand its production capabilities and prepare for commercial launch. EIC also invested $15.4 million (€14.8 million) in Spanish startup MOA Foodtech, while the French government and public investment bank Bpifrance funded Standing Ovation to scale up precision fermentation-made casein.

Interest seems to be continuing into 2025, with Germany’s Formo announcing it had received a $36 million (€35 million) venture loan from the European Investment Bank, and Dutch startup Vivici securing $33.7 million (€32.5 million), in part to establish long-term manufacturing capabilities.

Plant-based deals reveal an immature sector

Europe’s plant-based food sector appeared to experience an exceptional fundraising year in 2023, driven mainly by significant investments in publicly traded companies. Most prominently, Swedish plant-based dairy company Oatly secured $425 million (€391 million) across two large deals.

Taking these funding rounds into account creates a misleading impression that the whole sector saw a dip in funding in 2024. However, when excluding these outlier deals and focusing on the privately-held companies that make up most of the plant-based ecosystem, European investment rose by 37% to $181 million (€167 million).

Innovative companies working in this space are continuing to see the results of their R&I work pay off.

Spain’s Heura received $43 million (€40 million), helping it develop products that more closely match consumers’ expectations on taste and nutrition, France’s La Vie raised $27 million (€25 million) to improve its plant-based pork and develop new products, and the UK’s THIS received $25.5 million (€23.5 million) to expand its product range.

GFI’s State of the Industry Report covering the global plant-based sector also highlights that Europe is the world’s largest market for these foods. Euromonitor data covering the region suggests retail sales of plant-based meat, seafood, milk, yoghurt and ice cream were worth $9.7 billion (€8.9 billion) in 2024.

Cultivated meat companies scaling up

Figures related to European companies developing cultivated meat products and ingredients were also skewed by large deals in 2023, contributing to an overall 59% decline in funding to $52 million (€48 million) in 2024.

Many of the companies that saw large funding rounds last year were focused on preparing for market entry, such as the Netherlands’ Mosa Meat, which raised $42.9 million (€40 million), while Meatable secured $8.4 million (€7.6 million) from the Netherlands Enterprise Agency.

It’s positive to see a strong theme of commercialisation running through the latest alternative protein investments, but for Europe’s sector to meet its true potential, it must diversify its funding sources.

New funding mechanisms necessary for commercialisation

Europe lacks the infrastructure needed to scale up production of alternative proteins, and building a demo or commercial-scale facility can cost between €15 million and €250 million – an unrealistic target for startups to raise from venture capital.

To reap the benefits that protein diversification can offer Europe, governments and organisations such as philanthropic foundations should develop a range of innovative finance mechanisms to support this growing ecosystem – a subject explored by our new report.

These measures include blended finance models, such as guarantees, grants, concessional loans, leasing arrangements, and market-shaping schemes. Public bodies can also provide support through public procurement policies to increase the adoption of plant-based foods, including food biotech in existing carbon credit schemes, and reduce costs by supporting related industries, such as companies producing fermentation tanks.

Measures such as this can help raise confidence in the sector, attract more private investments and put these sustainable foods within the reach of European consumers, helping to boost food security, reduce climate emissions and support a shift towards more nature-friendly farming.

Read about our methodology for analysing investments in alternative protein companies.

All dollar to euro conversions carried out using 2024’s average exchange rate of 0.9243.

Author

Helene Grosshans

Infrastructure Investment Manager

Helene works to mobilise more capital into the alternative protein industry to finance infrastructure projects.