Affordability is a key sales driver for plant-based foods – but low prices aren’t sufficient for success

GFI Europe analysed Circana retail sales data for six European countries (France, Germany, Italy, the Netherlands, Spain and the UK) and up to six plant-based product categories (plant-based meat, seafood, milk and drinks, cheese, yoghurt and cream). Plant-based foods have enormous potential to help Europe build a more sustainable and resilient food system, if they can meet consumer expectations. Retail sales data can help to highlight where the sector is making progress, and where further investment is needed.

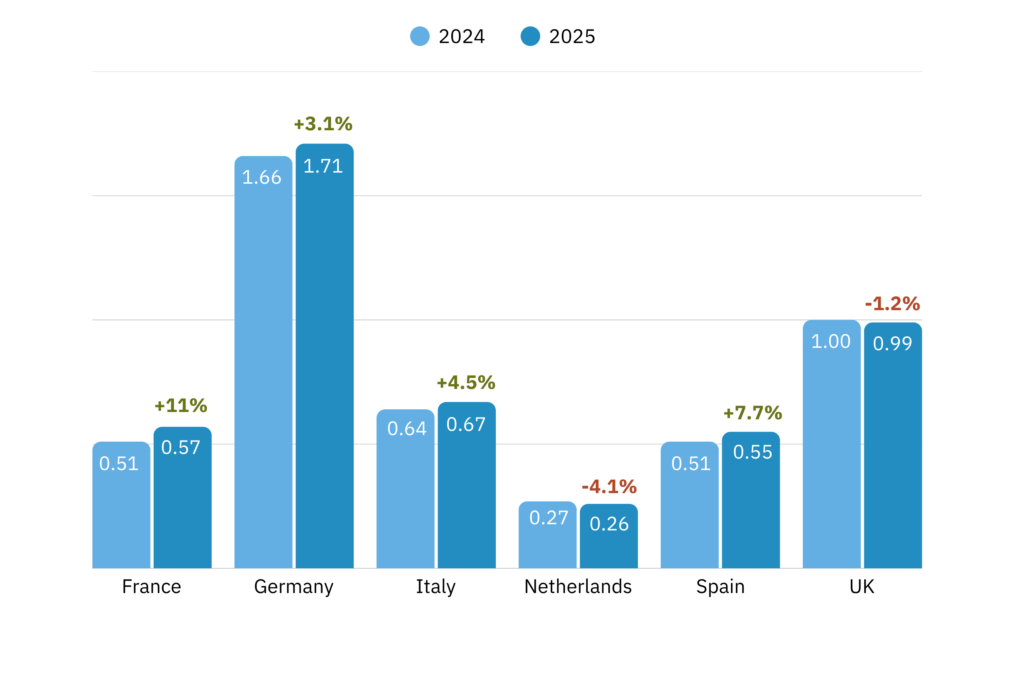

Plant-based food sales value across European countries (in € billions)

Plant-based food sales value

2024

2025

2024–25 change

France

€513,229,305

€571,688,728

11.0%

Germany

€1,658,996,254

€1,709,650,392

3.1%

Italy

€640,009,323

€668,778,552

4.5%

Netherlands

€270,462,775

€259,447,906

-4.1%

Spain

€506,677,987

€545,659,204

7.7%

United Kingdom

€1,005,711,656

€993,423,649

-1.2%

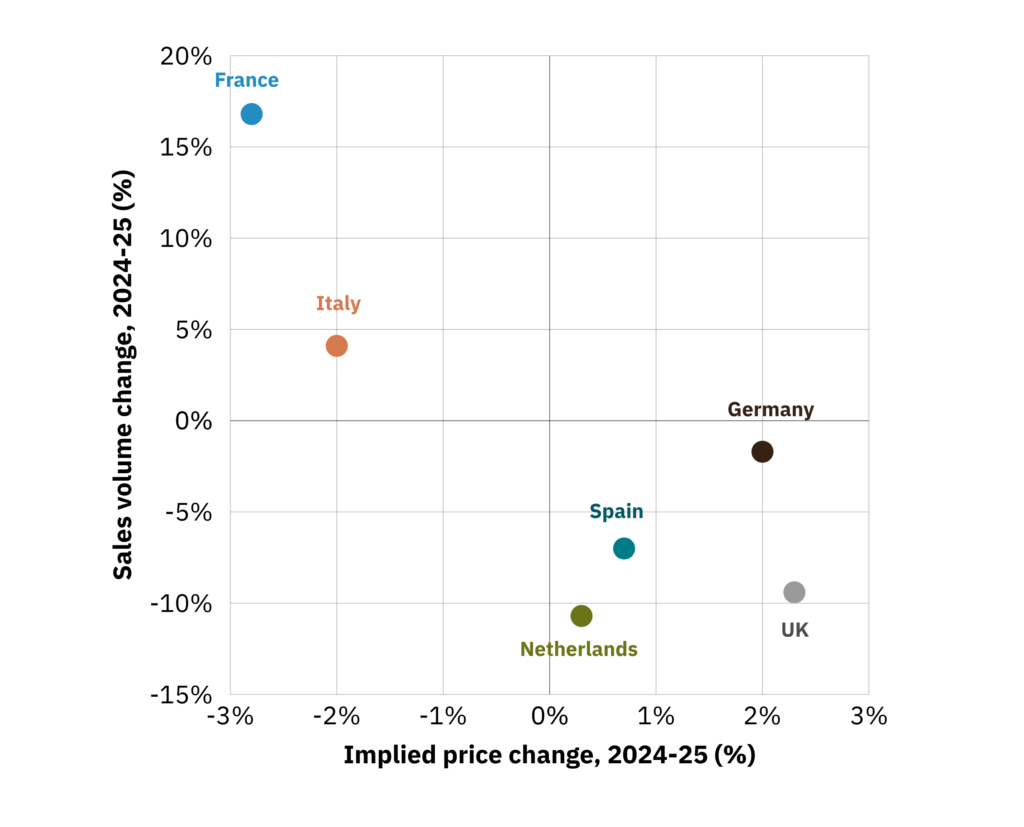

While performance varied across markets and product categories, prices were a key determinant of sales growth across many markets in 2025. In Italy, plant-based meat and milk saw both falling prices and rising sales. In France, plant-based meat prices fell, and sales volume grew by 17%. In Spain, plant-based milk – the category with the lowest price premium (18% on average, and just 7% for private-label options) – is by far the most successful.

Plant-based meat sales volume vs plant-based meat price change, 2024-2025

Plant-based meat 2024–25 change

Sales volume

Price

France

16.8%

-2.8%

Germany

-1.7%

2.0%

Italy

4.1%

-2.0%

Netherlands

-10.7%

0.3%

Spain

-7.0%

0.7%

United Kingdom

-9.4%

2.3%

Growing sales of tofu, tempeh and seitan also point to the importance of price, and may reflect consumer concerns about processing. This category grew by almost 30% in Germany and the Netherlands in 2025, with tofu costing a third of the price of branded plant-based meat in the Netherlands. Yet Dutch consumers bought 3.6 times more plant-based meat than tofu, tempeh and seitan combined in 2025 – demonstrating that products that replicate the taste, texture or format of conventional meat are reaching a wider audience.

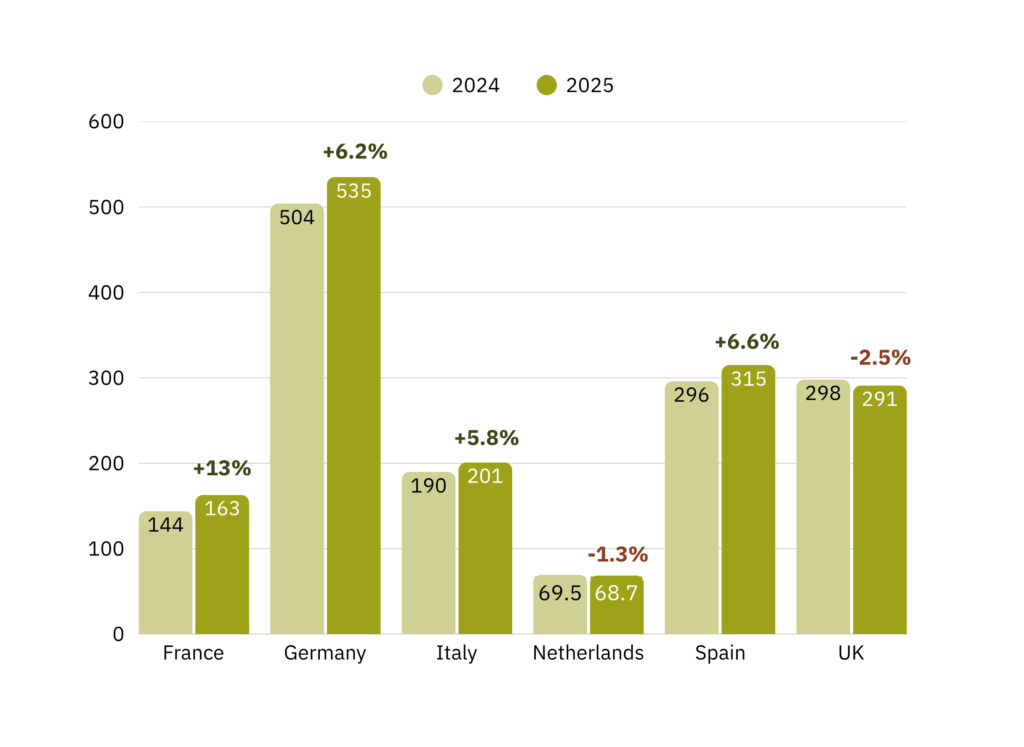

Plant-based foods sales volume across European countries (in millions kg)

Plant-based food sales volume (kg)

2024

2025

2024–25 change

France

143,593,111

162,636,253

13.0%

Germany

503,716,528

534,912,859

6.2%

Italy

189,649,922

200,699,751

5.8%

Netherlands

69,627,044

68,693,825

-1.3%

Spain

295,656,701

315,257,073

6.6%

United Kingdom

298,164,631

290,582,850

-2.5%

The continued dominance of more expensive branded products in most countries also suggests consumers are prioritising taste and quality. In the UK, more expensive plant-based milk options, including oat and barista-style varieties, performed well in 2025 – suggesting that taste and product performance were decisive factors for consumers.

Research suggests the EU’s plant-based market could be worth €45.5 billion by 2040 and support 350,000 jobs, while reducing Europe’s reliance on imports and helping to build a more sustainable food system. But as long as plant-based options represent a compromise on either taste or price, sustained growth will remain out of reach. To unlock their potential, governments and industry must invest now in the research and infrastructure needed to make plant-based options delicious and affordable.

Click each country tab below to find more details about its plant-based trends and links to the full reports and analysis in both English and the local language.

In France, plant-based food sales across five categories grew 13% in volume in 2025, reaching €572 million – a 11% increase from €513 million in 2024.

Plant-based meat saw the strongest growth, up 16.8% in volume and 13.5% in value in 2025, while milk and drinks led the French plant-based market with €255 million in sales.

Despite strong growth – a typical marker of a young market – plant-based foods are yet to break into the mainstream in France. Plant-based options accounted for 5.5% of all milk sold and 2.1% of all chilled packaged meat sold in French retailers in 2025.

To reach mainstream audiences, prices must come down and taste must continue to improve. In 2025, plant-based options were 25% more expensive per kg than animal-based meat and 68% more expensive per litre than dairy milk.

A recent analysis by Systemiq suggests France’s alternative protein market could be worth €10 million by 2040, supporting 64,000 jobs, while increasing resilience and reducing the country’s reliance on imports– only if policymakers and industry invest in the research and infrastructure needed to scale.

Overview of plant-based food sales by category in France, 2023-2025

Sales value

Unit sales

Sales volume

2025, € million

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Chilled meat

171.3

13.5%

32.1%

58.2

19.4%

42.5%

10.1

16.8%

32.1%

Milk and drinks

255.1

13.4%

20.6%

122.4

15.4%

21.0%

122.3

14.8%

19.7%

Cheese

12.2

5.4%

21.5%

4.5

6.4%

23.2%

0.7

5.9%

21.7%

Yoghurt

114.3

6.6%

9.8%

52.6

7.0%

8.6%

24.8

6.8%

9.0%

Cream

18.9

1.9%

9.2%

11.9

5.2%

12.2%

4.7

4.0%

14.4%

Total

571.7

11.4%

21.0%

249.6

13.7%

21.9%

162.6

13.3%

18.5%

Bonus data on additional products that are not counted towards the plant-based total

Tofu, tempeh and seitan

8.0

20.9%

17.2%

3.0

25.4%

26.7%

0.7

22.7%

4.5%

Plant-based sales and growth rates across five product categories in France, branded vs private label, 2023-2025

Germany remains the largest plant-based market in Europe, with sales across six categories reaching €1.71 billion in 2025 – up 6.2% in volume.

Consumer interest is widespread, as 31% of households bought plant-based meat and 38% bought plant-based milk at least once in 2025.

Plant-based meat sales levelled off, with volume declining slightly by 1.7% and value holding roughly steady at €751 million. Meanwhile, tofu, tempeh and seitan grew 30% in volume, although German consumers still bought 3.7 times more plant-based meat than these three foods combined.

Plant-based milk is a standout success, valued at €632 million in 2025 and growing 7.7% in volume – representing 9.2% of all milk sold in German retailers. Private-label options – now cheaper than private-label dairy milk – made up 60% of sales volume. On average, plant-based milk remained 10% more expensive per litre than animal-based options in 2025, but this is largely because plant-based options are taxed at 19% (vs 7% for cow’s milk).

Smaller categories highlight the need for investment in taste and innovation. Plant-based cheese sales volume remained steady overall, but sales of private-label options grew as prices fell. Plant-based seafood saw a significant decline in sales volume, with early research indicating that the category does not yet meet consumer expectations on taste and texture.

Overview of plant-based food sales by category in Germany, 2023-2025

Sales value

Unit sales

Sales volume

2025, € million

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Meat

750.8

0.2%

4.6%

347.2

-0.5%

6.7%

52.3

-1.7%

4.9%

Seafood

14.1

-22.0%

-41.4%

5.3

-19.2%

-41.1%

1.0

-29.4%

-47.1%

Milk and drinks

632.4

8.1%

12.1%

417.8

7.3%

14.3%

416.2

7.7%

16.2%

Cheese

85.5

-7.4%

-21.8%

48.4

-2.9%

-3.2%

7.5

-0.5%

-2.3%

Yoghurt

173.9

9.8%

8.3%

113.7

6.5%

15.2%

47.0

7.8%

15.5%

Cream

53.0

-4.8%

0.0%

51.4

-5.9%

4.4%

11.0

-6.7%

1.8%

Total

1709.7

3.1%

5.0%

983.9

2.9%

9.6%

534.9

6.2%

14.1%

Data on additional products that are not counted towards the plant-based total

Tofu, tempeh and seitan

95.1

28.9%

55.1%

41.5

28.1%

49.4%

14.0

29.7%

53.2%

Plant-based sales and growth rates across six product categories in Germany, branded vs private label, 2023-2025

Sales value

Unit sales

Sales volume

2025, € billion

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Branded

1.15

3.5%

3.5%

542.2

2.8%

3.8%

238.2

4.7%

4.7%

Private label

0.56

2.1%

8.1%

441.5

3.0%

17.6%

296.7

7.6%

22.9%

Household purchase patterns for plant-based foods in Germany, 2023-2025

In Italy, plant-based food sales across five categories reached €669 million in 2025, with all categories growing and total volume up 5.8%. Plant-based milk is the dominant category, making up 8.5% of all milk sold in Italian retailers.

Falling prices are driving growth. Average costs for plant-based meat, milk and cream declined slightly between 2023 and 2025 despite broader food inflation, with more affordable private-label products seeing faster sales volume growth (19.4%) than branded options (7%) over the same period.

However, branded products still account for the majority of sales and saw accelerated growth in sales volume last year, suggesting taste and perceived quality remain key purchase drivers.

Italians bought 4.3 times more plant-based meat than tofu, tempeh and seitan, reinforcing that products replicating the taste and format of meat have the broadest appeal.

A recent analysis by Systemiq suggests Italy’s alternative protein market could be worth nearly €6 billion and support 31,000 jobs by 2040 – if policymakers and industry leaders invest in the research and infrastructure needed to improve taste and bring prices further down.

Overview of plant-based food sales by category in Italy, 2023-2025

Sales value

Unit sales

Sales volume

2025, € million

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Meat

233.9

2.0%

17.4%

95.9

5.0%

26.3%

17.8

4.1%

21.1%

Milk and drinks

341.7

5.6%

8.4%

180.2

6.6%

13.2%

170.5

6.2%

12.4%

Cheese

25.9

17.1%

69.7%

10.7

16.6%

58.5%

1.6

15.6%

65.9%

Yoghurt

60.5

3.7%

6.1%

43.6

5.2%

9.3%

9.5

1.9%

1.7%

Cream

6.9

3.6%

-8.3%

5.2

5.0%

-0.5%

1.4

2.9%

-2.7%

Total

668.8

4.5%

12.5%

335.7

6.2%

16.9%

200.7

5.8%

12.7%

Data on additional products that are not counted towards the plant-based total

Tofu, tempeh and seitan

40.1

22.0%

63.2%

19.4

25.7%

81.6%

4.1

23.9%

72.7%

Plant-based sales and growth rates across five product categories in Italy, branded vs private label, 2023-2025

In the Netherlands, plant-based food sales across five categories were worth €259 million in 2025, a 4.1% decline in value and a 1.3% decline in sales volume.

Despite this decline in sales, the Netherlands remains one of Europe’s most mature plant-based markets, with strong institutional support for protein diversification and the third-highest per capita spend on plant-based foods in 2025 of the six countries in this report series.

Plant-based meat – the largest category by value – saw sales volume fall by 10.7% in 2025, driven by a 15.8% drop in sales of branded products. Private-label options, meanwhile, saw only a 2% decline in sales volume in 2025, following a 6.7% increase in 2024. This difference in performance reflects diverging prices – with private-label products becoming cheaper over time, while branded prices continued to increase.

Plant-based milk sales value grew 4% to €93.5 million and volume remained steady, representing 8.9% of all milk sold in Dutch retailers in 2025. Growth in premium segments like barista-style milk suggests that better product performance can drive sales.

Tofu, tempeh and seitan saw 27% growth in both value and volume in 2025. However, Dutch consumers still bought 3.6 times more plant-based meat than these three products combined, confirming that products replicating the taste and format of meat retain the broadest appeal.

To reach their world-leading protein diversification targets, Dutch policymakers, producers and retailers must continue to invest in improving the taste and reducing the cost of plant-based options.

Overview of plant-based food sales by category in the Netherlands, 2023-2025

Sales value

Unit sales

Sales volume

2025, € million

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Meat

108.1

-10.5%

-17.4%

41.0

-12.1%

-19.0%

8.0

-10.7%

-16.7%

Milk and drinks

93.5

4.0%

-0.3%

49.0

2.3%

-1.9%

46.6

0.7%

-3.8%

Cheese

10.6

0.4%

-7.2%

4.9

2.2%

-0.7%

0.9

3.6%

1.1%

Yoghurt

41.7

-4.6%

-7.2%

21.7

-3.8%

3.8%

12.2

-2.9%

2.1%

Cream

5.5

0.1%

2.6%

4.1

4.0%

4.4%

0.9

5.1%

6.2%

Total

259.4

-4.1%

-9.4%

120.8

-4.1%

-7.4%

68.7

-1.3%

-4.4%

Bonus data on additional products that are not counted towards the plant-based total

Tofu, tempeh and seitan

13.7

27.3%

41.3%

6.9

26.0%

35.8%

2.2

27.1%

34.9%

Plant-based sales and growth rates across five product categories in the Netherlands, branded vs private label, 2023-2025

In Spain, plant-based food sales were valued at €546 million in 2025, up 6.6% in sales volume, with growth driven by the milk and yoghurt categories.

Plant-based milk reached €355 million in 2025 (up 5.8% in volume). Plant-based options were bought by almost half of Spanish households in 2025, and represented 10.4% of all milk sold in Spanish retailers.

Plant-based yoghurt saw sales volume jump 22.8%, reaching €118 million in value in 2025.

The success of plant-based milk – where private-label products cost just 7% more per litre than private-label dairy milk in 2025 – and the growth of innovative barista options show that competitive pricing and improved taste can drive mainstream adoption.

Plant-based meat is being held back by price. Sales volume fell 7% in 2025 as prices rose, with plant-based meat costing more than twice as much as animal-based meat. One in five Spanish households bought plant-based meat in 2025, suggesting widespread interest, but price remains a barrier to repeat purchases.

A recent analysis by Systemiq suggests Spain’s alternative protein market could be worth €6.7 billion and support 34,000 jobs by 2040 – if policymakers and industry leaders invest in the research and infrastructure needed to improve taste and bring prices further down.

Overview of plant-based food sales by category in Spain, 2023-2025

Sales value

Unit sales

Sales volume

2025, € million

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Meat

65.3

-6.3%

-7.0%

22.2

-7.3%

-5.6%

4.2

-7.0%

-7.4%

Milk and drinks

354.9

5.5%

8.2%

231.6

4.6%

10.0%

288.5

5.8%

12.6%

Cheese

7.4

-0.1%

10.8%

2.4

-2.6%

5.1%

0.4

-3.1%

2.8%

Yoghurt

118.0

26.7%

53.5%

55.8

23.8%

50.5%

22.1

22.8%

43.3%

Total

545.7

7.7%

13.3%

312.0

6.6%

14.1%

315.3

6.6%

13.9%

Data on additional products that are not counted towards the plant-based total

Tofu and seitan

20.3

2.2%

12.0%

9.8

3.6%

15.6%

3.0

8.6%

20.3%

Plant-based sales and growth rates across four product categories in Spain,branded vs private label, 2023-2025

Sales value

Unit sales

Sales volume

2025, € million

2024-25 change

2023-25 change

2025, million units

2024-25 change

2023-25 change

2025, million kg

2024-25 change

2023-25 change

Branded

314.0

10.8%

16.7%

145.0

10.2%

15.7%

119.8

6.6%

4.1%

Private label

231.7

3.7%

8.9%

167.0

3.5%

12.7%

195.5

6.6%

20.9%

Household purchase patterns for plant-based foods in Spain, 2023-2025

In the UK, plant-based food sales across six categories were worth £848 million (€993million) in 2025.

Seafood, soft and snacking cheese, and yoghurt saw volume growth in 2025.

Plant-based meat sales volume declined by 9.4%, although the proportion of sales value captured by discounter stores not covered by Circana’s data increased, suggesting that this decline may be overstated.

Non-analogue meat alternatives such as bean burgers saw an 11.4% decline in sales volume in 2025, while tofu, tempeh and seitan sales volume grew by 16.8%. The sales volume of plant-based meat was 90% higher than that of non-analogue meat alternatives, tofu, tempeh and seitan combined. This shows that despite falling sales, products that offer a similar taste, texture or format to conventional meat retain broader appeal among UK consumers.

Plant-based milk sales volume contracted slightly, although category value remained steady in 2025. Oat milk remained the most popular base ingredient and retained steady sales volume, despite being more expensive than options like soy, almond and coconut. Premium barista-style products also saw 10% growth in sales volume. This suggests that taste and product performance are key factors for UK plant-based milk consumers.

The UK Government recently recognised alternative proteins as a “major opportunity” for its Good Food Cycle, helping to contribute to economic growth and improving public health. Ministers should use policy levers, such as a mandatory ‘protein split’ target and updated national dietary guidelines, to unlock the full health and environmental potential of plant-based foods.

Overview of plant-based food sales in UK supermarkets excluding discounters, by category, 2024-2025

Sales value

Unit sales

Sales volume

2025, £ million

2024-25 change

2025, million units

2024-25 change

2025, million kg

2024-25 change

Meat

294.6

-7.3%

125.9

-8.6%

30.5

-9.4%

Seafood

5.9

8.9%

2.3

8.5%

0.5

13.7%

Milk and drinks

419.3

0.5%

241.4

-2.2%

236.1

-2.2%

Cheese (soft and snacking)

14.0

12.6%

5.8

10.0%

0.9

10.1%

Yoghurt

102.3

10.0%

55.8

8.1%

20.8

4.7%

Cream

11.8

-4.7%

7.9

-6.7%

1.9

-6.8%

Total

847.8

-1.2%

439.1

-2.9%

290.6

-2.5%

Data on additional products that are not counted towards the plant-based total

Tofu, tempeh and seitan

52.1

14.6%

23.4

20.8%

6.5

16.8%

Plant-based sales and growth rates across six product categories in UK supermarkets excluding discounters, branded vs private label, 2024-2025

Sales value

Unit sales

Sales volume

2025, £ million

2024-25 change

2025, million units

2024-25 change

2025, million kg

2024-25 change

Branded

764

-0.6%

379

-1.9%

241

-1.7%

Private label

84

-6.4%

60

-8.6%

49

-6.5%

Household purchase patterns for plant-based foods in the UK, 2023-2025

“Across leading European markets, we’re seeing clear evidence that consumers are interested in plant-based foods, but price and taste continue to shape purchasing decisions. While the price gap with animal products is closing in many categories, affordability alone is not sufficient for growth: a good eating experience is also crucial to reach larger audiences.”

Helen Breewood, Senior Market and Consumer Insights Manager

About the data

Retail sales trends in this series of reports are based on data gathered by Circana from retailers. The data has been analysed by the Good Food Institute Europe.

The coverage varies between countries in terms of retailers (eg, whether discounters are covered or not), product category definitions, and precise time periods, so the totals for each country are not directly comparable to those for other countries. Full details of the coverage for each country are available in each report.

Tofu, tempeh and seitan are not counted towards the plant-based totals for each country, because they are not typically marketed as direct substitutes for meat. They are included for comparison.

The data does not cover sales in the foodservice sector, such as in restaurants or fast food outlets.

This publication also draws on household panel data from the NIQ Panel On Demand Homescan. This tracks food purchases made by a panel of consumers to offer a complementary viewpoint to the Circana retail sales data. Data is nationally representative of the population within each country and covers “take-home” shopping, ie, food items purchased in a retail environment (including discounters) and then brought home. It does not cover items consumed outside of the home, or foodservice sales. The panel sizes are 12,000 households for Spain, 25,000 for Germany and 30,000 for the UK.

Note that the data in these reports is not directly comparable to previous publications from GFI Europe, due to ongoing refinement and improvement of the datasets from both Circana and NIQ.

Finnish retail sales data A 2026 report by Plant Based Food Finland – Pro Vege provides a comprehensive overview of the Finnish plant-based food retail market including plant-based meat, pulses and non-dairy categories, their sales development in 2025, and key consumer trends. Read the report here.

Polish retail sales data A 2025 report by the Polish Plant-Based Food Producers Association presents retail sales trends of plant-based foods in Poland up to June 2024. Read the report here.