Plant-based retail sales in six European countries, 2022 to 2024

Retail sales volumes of plant-based foods are growing in France, Germany, Italy and Spain, with cheaper private-label products driving much of the increase.

Image: Planted Foods AG

Read the reports

Containing full segment breakdowns and key insights.

Affordable private-label products are driving sales volume growth, but taste remains key

GFI Europe analysed Circana retail sales data for six European countries (France, Germany, Italy, the Netherlands, Spain and the UK) and up to six plant-based product categories (plant-based meat, seafood, milk and drinks, cheese, yoghurt and cream).

In France, Germany, Italy and Spain, rising sales volumes are being driven primarily by growth in private-label products (those sold under the brand of a retailer), which are, in most cases, cheaper than branded products. These affordable options – particularly plant-based milk and drinks, which are approaching mainstream status in several countries – appeal to a wider consumer base.

However, in some categories, relatively expensive branded products are driving sales. This suggests that, as the rate of food inflation has eased, existing plant-based consumers are increasingly focused on factors like taste, ease of preparation or perceived quality. Early adopters of categories such as plant-based meat and cheese may be willing to pay a premium for options that taste good and align with their values. But reaching both taste and price parity with animal products will be essential for plant-based foods to reach a wider audience and deliver their full benefits for the environment and public health.

Our separate consumer research in the UK and Germany found that half of consumers want to eat more plant-based foods or less meat and dairy. However, consumers perceive plant-based foods as falling short of animal-based foods in key areas such as taste, availability, ease of cooking and value for money. By continuing to improve the taste and price of plant-based foods so that they meet the expectations and needs of a wide range of consumers, the plant-based sector can tap into this large potential market.

Countries at a glance

France: Private-label products are driving sales volume growth, particularly for plant-based milk and drinks. Private-label sales rose by 8.9% in 2024. The strongest growth was seen in plant-based cheese, up 19.5% in volume in 2024.

Italy: Private-label sales volume increased by 11.8% in 2024, versus 1.9% growth for branded. The strongest growth was in plant-based cheese, up 43.2% in volume from 2022 to 2024.

Spain: Private-label sales volume grew by 13.1% in 2024, versus 2.9% growth for brands. Plant-based yoghurt sales volume rebounded, up 16.7% in 2024.

46% of households bought plant-based milk and 22% bought plant-based meat at least once in 2024.

Germany: 37% of households bought plant-based milk and 32% bought plant-based meat at least once in 2024. Private-label sales were up 13.9% in volume in 2024, with branded sales volume staying level.

Netherlands: Plant-based yoghurt rebounded, with 4.9% growth in sales volume in 2024. In plant-based meat, cooking ingredients like mince were more resilient than centre-plate formats.

UK: Certain categories bucked the trend, as sales volume rose 10.4% for barista milk, 6.3% for yoghurt, 3.3% for cream and 2.2% for seafood in 2024.

32% of households bought plant-based meat and 32% bought plant-based milk at least once in 2024.

Country-level reports

Click each country tab below to find more details about its plant-based trends and links to the full reports and analysis in both English and the local language.

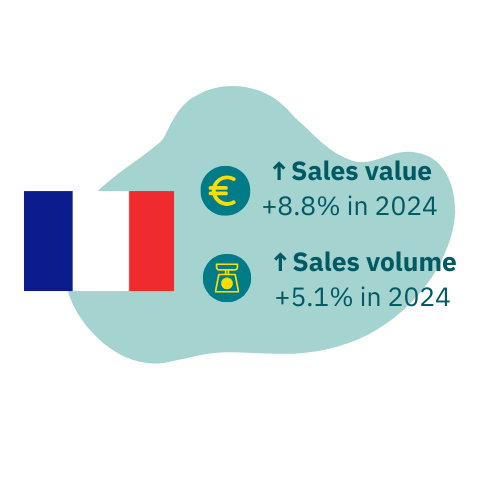

The French retail market across five categories of plant-based food was valued at €537 million in 2024 – 8.8% higher than in 2023 and 20.5% higher than in 2022.

Sales volume growth accelerated between 2023 and 2024, possibly aided by falling inflation reducing pressures on consumer budgets.

All five plant-based categories grew in terms of sales value, unit sales and sales volume between 2023 and 2024, outperforming their animal-based equivalents in terms of percentage growth.

The strongest growth was seen in the emerging plant-based cheese category, where sales volumes were up by nearly half between 2022 and 2024, albeit from a low base.

Private-label products were particularly important in the plant-based milk and drinks category, which is the largest plant-based category in France, suggesting that affordability is important for reaching a wide market.

Relatively expensive branded products gained market share in the plant-based meat and yoghurt categories, and made up the majority of plant-based cheese sales. This suggests that, in these categories, consumers are also strongly driven by other factors in addition to price, such as taste and quality.

Plant-based sales summary by category, France, 2022-2024

For more insights, read the full report for France linked below, available in French and English.

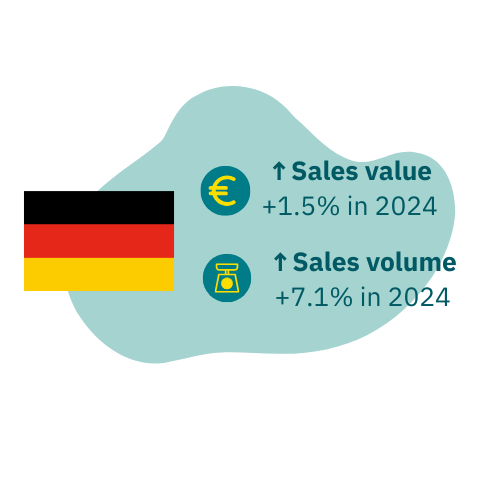

The German retail market across six categories of plant-based food was valued at €1.68 billion in 2024 – 1.5% higher than in 2023 and 6.8% higher than in 2022.

The levelling off in sales value reflects falling prices, as sales volume rose by 7.1% between 2023 and 2024 and by 13.5% between 2022 and 2024.

Sales volume grew between 2023 and 2024 in four of the six categories: meat, milk and drinks, yoghurt and cream.

Private-label products – those sold under the brand of a retailer – drove the growth in sales volume. They tend to have lower prices compared to branded products, which saw stable sales volume between 2023 and 2024.

Plant-based milk and drinks have become more affordable relative to animal-based milk – particularly in the private-label segment – which is likely to be driving the ongoing growth in sales volume in this already well-established category. However, plant-based milk options are still disadvantaged by the design of German VAT, which artificially makes them more expensive. Without this distortion of competition, this category could reach an even wider group of consumers.

Plant-based cream was 5% cheaper per kg than animal-basedcream in 2024, possibly driving increased sales.

Germany is the biggest plant-based market in Europe, with the highest per capita spend on plant-based foods out of the six countries in 2024, at €19.92 per person per year.

Plant-based sales summary by category, Germany, 2022-2024

Household purchase patterns for plant-based foods in Germany, 2022-2024

The totals in this year’s German report are not comparable to those in our previous publication, Germany plant-based food retail market insights: 2021 to 2023 with initial insights into the 2024 market. This is because the totals have been updated following a correction in the categorisation of the data from Circana. See the “About the data” section for more information.

For more insights, read the full report for Germany linked below, available in German and English.

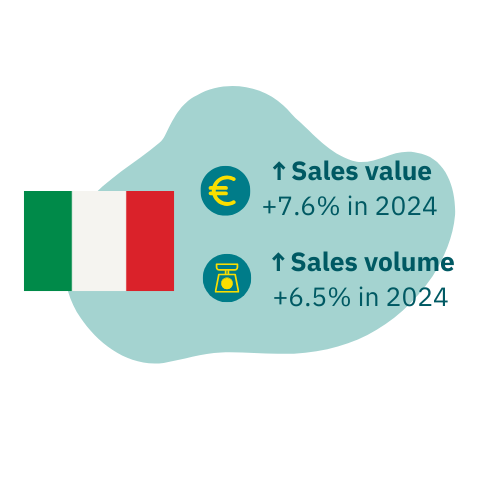

The Italian retail market across five categories of plant-based food was valued at €639 million in 2024 – an increase of 16.4% compared with 2022 and an increase of 7.6% compared with 2023.

Sales volume growth has accelerated, with the vast majority of the growth happening between 2023 and 2024.

Sales volume grew in three out of five plant-based categories between 2023 and 2024 (meat, milk and drinks, and cheese). Sales volume was level for plant-based yoghurt, and decreased for plant-based cream.

Plant-based cheese doubled in annual sales value between 2022 and 2024, driven by relatively expensive branded products.

High inflation in Italy’s food sector in 2022 and 2023 could explain the strong growth of relatively affordable private-label products, which saw a 17.4% rise in sales volume between 2022 and 2024, compared to steady sales volume (-1.5%) for branded options. Private-label products were particularly important in the plant-based meat and milk and drinks categories.

Plant-based sales summary by category, Italy, 2022-2024

For more insights, read the full report for Italy linked below, available in Italian and English.

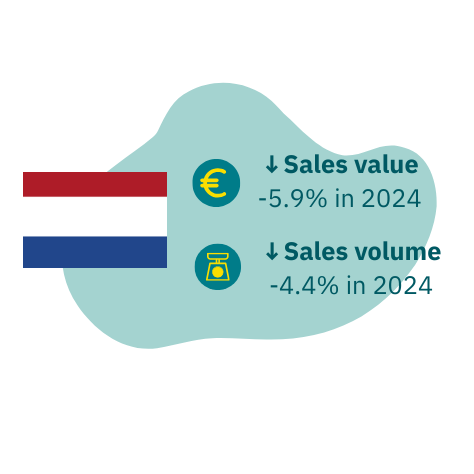

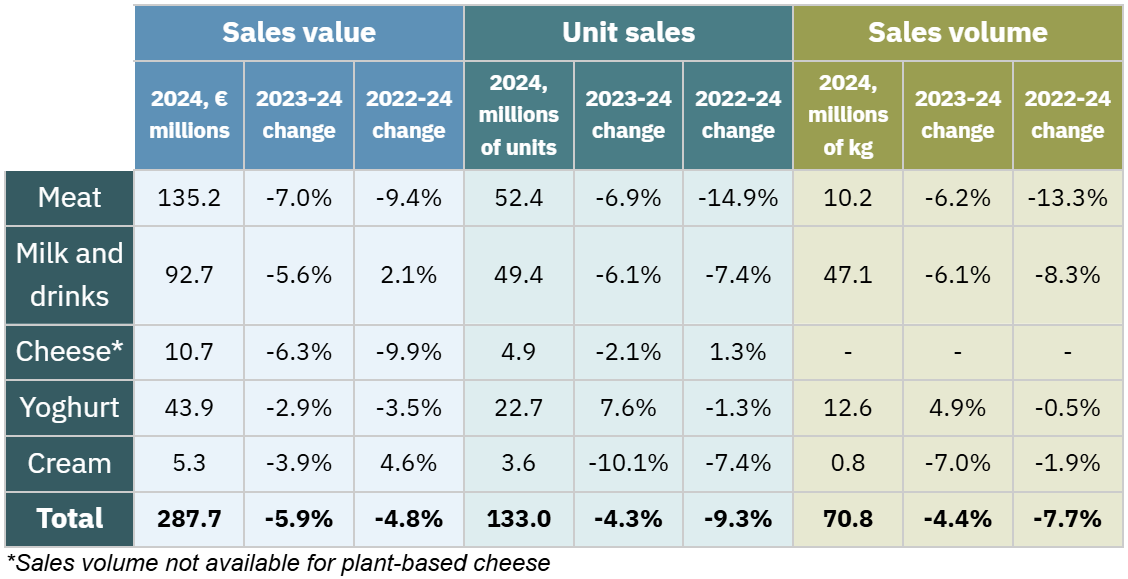

The retail market across five plant-based categories in the Netherlands was worth €288 million in 2024 – down 5.9% from 2023.

Overall unit sales and sales volume* fell steadily between 2022 and 2024, down by 4.3% and 4.4%, respectively, in 2024.

Nevertheless, in 2024, the Netherlands had the second-highest per capita spend on plant-based foods out of the six countries, at €15.78 per person per year.

Plant-based yoghurt rebounded, with 4.9% growth in sales volume in 2024 following a dip in 2023, possibly driven by falling prices.

Most of the fall in sales volume of plant-based milk and drinks came from significantly lower sales of chilled products, with sales of ambient products staying stable. Chilled plant-based milk has risen in price over time, while that of ambient plant-based milk remained level between 2023 and 2024, but it is not clear whether the increase came from the impacts of a new tax on some plant-based milks or from other factors such as energy costs.

In the plant-based meat category, options more likely to be used as part of a home-cooked recipe (like mince and strips) remained relatively resilient, while sales of centre-plate formats such as burgers and fillets fell.

*Excluding plant-based cheese, for which sales volume is not available.

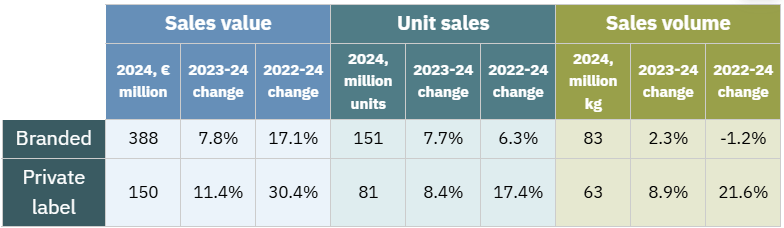

Plant-based sales summary by category, Netherlands, 2022-2024

For more insights, read the full report for the Netherlands linked below, or our summary blog exploring key trends, available in Dutch and English.

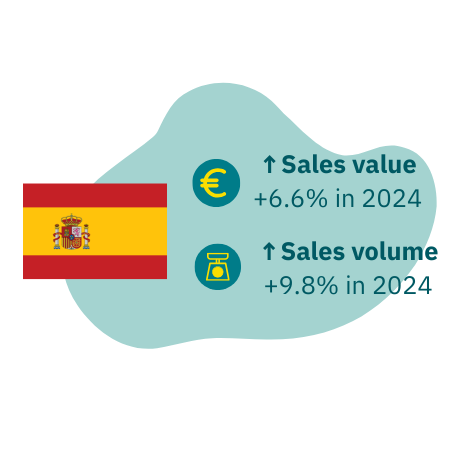

The Spanish retail market across four categories of plant-based food was valued at €491 million in 2024 – an increase of 6.6% relative to 2023 and 14.4% compared with 2022.

Sales volume was 286 million kg in 2024 – an increase of 9.8% on 2023 and 16.9% on 2022, showing that the growth in sales value can be attributed to an actual increase in demand, not to inflation. The annual rate of growth in sales volume increased between 2022 and 2024.

Household panel data from NIQ shows that, in 2024, more than one in five households purchased plant-based meat and almost half bought plant-based milk and drinks.

Sales volume grew in three out of four plant-based categories between 2023 and 2024. Plant-based meat was the only exception, with sales volume remaining roughly level over the same period.

Almost 10% of all milk sold in Spain in 2024 was plant-based. Plant-based milk and drinks have become more affordable over time,driven by the success of lower-cost private-label products.

Demand for plant-based yoghurt rebounded, with sales volume rising by 16.7% in 2024 following a dip in 2023. This growth was driven by relatively expensive branded products, suggesting that other factors such as taste and texture are also influencing consumers’ choices.

Plant-based sales summary by category, Spain, 2022-2024

Household purchase patterns for plant-based foods in Spain, 2022-2024

For more insights, read the full report for Spain linked below, available in Spanish and English.

The UK’s retail market (excluding discounter stores such as Aldi and Lidl) across six categories of plant-based food was valued at £904 million (€1.07 billion) in 2024, a fall of 4.1% from 2023.

The total sales volume in 2024 was 302 million kg – 3.2% lower than in the previous year – but the rate of decline has slowed.

Household panel data from NIQ shows that 31.8% of households bought plant-based milk at least once in 2024, up slightly on the previous year. 10.8% of UK households bought plant-based milk an average of once per month or more.

Sales of branded products were more resilient than those of private-label options, despite being more expensive, and several innovator brands bucked trends with significant growth. This suggests that factors such as taste and quality may be driving plant-based food sales in the UK.

Barista-style plant-based milk, which is designed to froth and be mixed into hot drinks without curdling, saw a 10.4% increase in sales volume in 2024. This shows the importance of making it easier for consumers to use plant-based products in the same way they would use animal-based equivalents.

Household panel data from NIQ shows that the proportion of sales value from discounter stores (such as Aldi and Lidl), which are not covered in the Circana retail sales data, rose between 2022 and 2024 for both plant-based meat and milk.

Plant-based sales summary by category, UK, 2022-2024

Household purchase patterns for plant-based foods in the UK, 2022-2024

For more insights, read the full report for the UK and the summary blog exploring key trends, both linked below and available in English.

“Europe’s plant-based retail market remains resilient, with increasing sales volumes across four countries in 2024. The rise of private-label options demonstrates that affordability is essential for reaching a wider market, and that plant-based foods are becoming more mainstream, with retailers investing in their own ranges.

“Nevertheless, the sector is facing challenges in some mature markets. The ongoing success of relatively expensive branded products in some product categories and countries indicates that price is not the only factor: the sector has the opportunity to reach more people by continuing to improve performance on both taste and price.”

Helen Breewood, Senior Market and Consumer Insights Manager

About the data

Retail sales trends in this series of reports are based on data gathered by Circana from retailers. The data has been analysed by the Good Food Institute Europe.

The coverage varies between countries in terms of retailers (eg, whether discounters are covered or not), product category definitions, and precise time periods, so the totals for each country are not directly comparable to those for other countries. Full details of the coverage for each country are available in each report.

The data does not cover sales in the foodservice sector, such as in restaurants or fast food outlets.

Note that the data in these reports is not directly comparable to previous publications from GFI Europe for several reasons, including:

The totals in this year’s Germany report are not comparable to those in our previous publication, Germany plant-based food retail market insights: 2021 to 2023 with initial insights into the 2024 market. This is because the totals have been updated following a correction in the categorisation of the data from Circana. This year’s dataset has been verified by cross-checking the totals within a new data format provided by Circana. The sales data for France, Italy, the Netherlands, Spain and the UK in our previous publications was not affected. Furthermore, the previous German report covered ready meals and desserts and puddings, which are not covered by this report.

Previous GFI Europe publications using Circana data covered additional product categories, including ready meals, desserts and ice cream for some countries. These categories are not included in the present series of reports.

Circana has improved the accuracy of its data collection system in Spain, most notably by incorporating and backdating Lidl’s census data. Previously, Circana’s sales data for Lidl were estimated. These changes have had the greatest effect in the plant-based meat category.

The item lists for the UK data have been refined, most notably in the plant-based milk and drinks and cheese categories.

The data is not comparable to previous retail sales reports based on retail sales data from NielsenIQ, as the methodology and category definitions differ from those of Circana.

This publication also draws on household panel data from the NIQ Panel On Demand Homescan. This tracks food purchases made by a panel of consumers to offer a complementary viewpoint to the Circana retail sales data. Data is nationally representative of the population within each country and covers “take-home” shopping, ie, food items purchased in a retail environment (including discounters) and then brought home. It does not cover items consumed outside of the home, or foodservice sales. The panel sizes are 8,000 households for Spain, 20,000 for Germany and 30,000 for the UK.