Europe’s plant-based food retail market grows as prices become more competitive, but good taste remains key

Data from six European countries show that the price gap between plant-based foods and their animal-based equivalents narrowed in most categories in 2025, leading to sales volume growth as products began to meet consumer expectations.

Find out more about what the data means for France, Germany, Italy, the Netherlands and Spain.

9 June 2026

Data from six European countries show that the price gap between plant-based foods and their animal-based equivalents narrowed in most categories in 2025, leading to sales volume growth as products began to meet consumer expectations.

New analysis of Circana retail sales data by GFI Europe shows the sales volume of plant-based foods increased in four of Europe’s six leading markets in 2025, with growth driven by improvements in affordability and taste.

Across France, Germany, Italy, the Netherlands, Spain and the UK, plant-based options generally remained more expensive per kg than their animal-based equivalents – but this price gap narrowed in 2025. In most cases, this was associated with growing sales volumes for plant-based foods. Across categories, total sales volume grew in France, Germany, Italy and Spain in 2025, while the Netherlands saw a slight decline and the UK recorded a contraction.

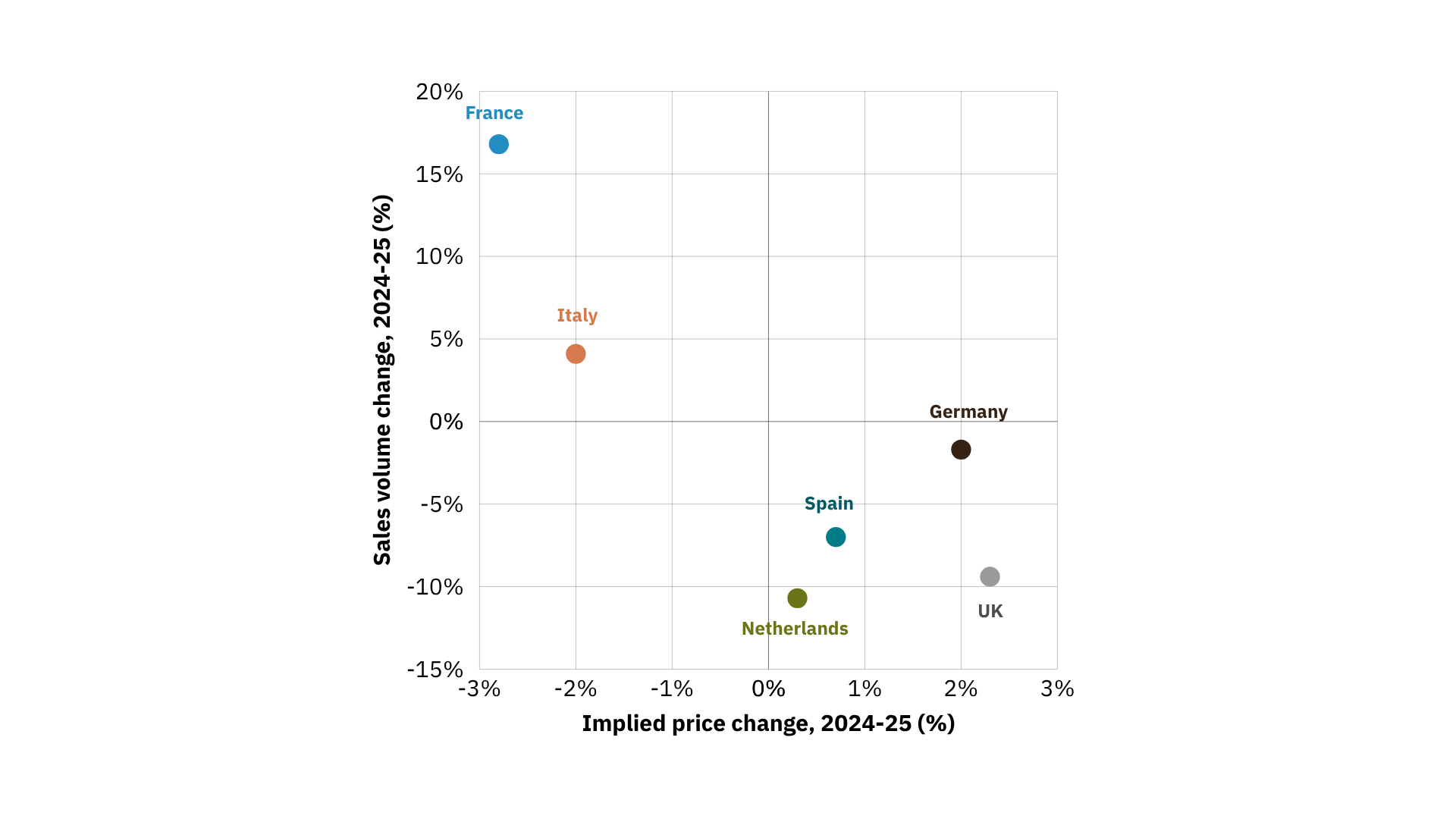

Plant-based meat sales volume vs plant-based meat price change, 2024-2025

The analysis highlights growing consumer interest in plant-based foods and provides important insights into how Europe can accelerate the shift towards a more sustainable, resilient and healthy food system. While affordability is a key driver of sales, long-term growth depends on delivering products that consumers actively want to buy again.

Helen Breewood, Senior Market and Consumer Insights Manager at GFI Europe, said: “Across leading European markets, we’re seeing clear evidence that consumers are interested in plant-based foods, but price and taste continue to shape purchasing decisions. While the price gap with animal products is closing in many categories, affordability alone is not sufficient for growth: a good eating experience is also crucial to reach larger audiences.”

Affordability is important, but not sufficient

The data suggests that affordability is an important factor shaping sales performance across all six markets, although it is not sufficient for success, and there are notable exceptions where premium segments perform better.

In Italy, plant-based meat and milk recorded sales growth while average prices declined slightly. In France, plant-based meat prices fell and sales volume increased by almost 17%. In Spain, plant-based milk – the category with the smallest price gap – remains by far the largest and most successful plant-based category, accounting for more than one in 10 litres of milk sold in Spanish retailers. These trends indicate that smaller price premiums may be driving growth in some categories and markets.

The growing popularity of tofu, tempeh and seitan also points to affordability and may reflect consumer interest in less processed foods. Sales volumes of these products increased by almost 30% in both Germany and the Netherlands in 2025. In the Netherlands, tofu costs roughly one-third as much as branded plant-based meat products.

Yet lower prices alone do not guarantee success. Despite the significant price difference, people across all six countries purchased significantly more plant-based meat than tofu, tempeh and seitan combined, indicating that products that replicate the taste, texture or format of conventional meat are reaching a wider audience.

In the UK, more expensive plant-based milk options, including oat and barista-style varieties, performed well in 2025 – suggesting that taste and product performance were decisive factors for consumers.

The continued dominance of branded products in many markets also suggests that existing plant-based consumers are willing to pay more when products better meet expectations on taste, texture and overall quality. However, products that represent a compromise on either taste or price are unlikely to achieve widespread adoption.

Plant-based milk shows how products can reach the mainstream

Plant-based milk remains the most mature category across all six countries analysed and demonstrates what’s possible for the sector.

Plant-based milk now accounts for between 7% and 10% of all milk sold in Germany, Italy, Spain and the Netherlands. In Spain, almost half of households purchased plant-based milk in 2025, while 38% of German households did the same.

Strong taste, functionality and continued innovation have helped drive adoption, with barista-style products now making up around a fifth of the range in several markets. At the same time, retailer investment in private-label products has helped reduce prices and make plant-based milk accessible to more consumers.

Germany provides a striking example. Private-label plant-based milk is now cheaper than private-label dairy milk, despite being taxed at 19%, compared with 7% for dairy milk. If policymakers were to remove this tax disadvantage, average prices for plant-based options would be roughly the same as dairy milk.

The category’s success demonstrates how investment in product development and affordability can help to make sustainable food choices mainstream.

Price was a factor in plant-based meat’s mixed performance

Plant-based meat continues to attract substantial consumer interest and remains one of the largest categories across Europe. In France, it was the fastest-growing category, with sales volume rising by 16.8% as prices fell. In Germany and the UK, 31% of households purchased plant-based meat in 2025, while one in five Spanish households did the same.

However, high prices continued to limit growth. In Spain, sales volume fell by 7% as prices rose, with plant-based meat costing more than twice as much as conventional meat in 2025. The Netherlands saw a similar decline, driven largely by a drop-off in sales of higher-priced branded products. Prices also rose in the UK, where plant-based meat in supermarkets (excluding discounters) contracted significantly, while separate data from NIQ suggested a shift towards discounter stores.

These findings point to a significant opportunity. If producers can continue improving taste while bringing prices closer to those of conventional meat, plant-based meat could play a much larger role in achieving crucial climate goals and improving public health, without requiring consumers to give up familiar dishes.

Investing in better and more affordable products could unlock major benefits

Across all six markets, consumer interest in plant-based foods is strong. The challenge is turning that interest into regular purchasing habits, as well as reaching new audiences.

The data shows that most plant-based categories are becoming more affordable relative to their animal-based equivalents, and that in most cases this has been associated with growth in sales volume. However, there are exceptions where narrower price gaps have not led to rising sales, and where more premium products have outperformed cheaper options. This shows that both taste and price are important to consumers, and for further growth, products must not require consumers to compromise on either.

Further investment in research, innovation and manufacturing capacity is essential to close those gaps. Governments and the food industry can support progress by investing in research to improve taste and texture, and building the infrastructure needed to scale production and lower prices.

The potential rewards extend far beyond retail sales. A larger European plant-based sector could help to reduce emissions from food production, strengthen food security, support public health goals and create new economic opportunities.

As the success of plant-based milk shows, when products are delicious, affordable and widely available, consumers will make sustainable choices part of everyday life. Research suggests the EU’s plant-based market could be worth €45.5 billion by 2040 and support 350,000 jobs, while reducing the bloc’s reliance on imports – but only if governments invest.