Alternative protein innovation priorities

Explore the results of our market research to uncover commercial white spaces, research gaps, technological needs, and investment priorities at each stage of the plant-based, cultivated meat and fermentation value chain.

Why advance alternative proteins in Europe?

Alternative proteins – spanning plant-based, cultivated and fermentation-made meat, eggs, dairy and seafood – are on the rise across Europe and consumers are hungry for more.

Retail sales of plant-based foods across Europe reached €5.8 billion in 2022 – 6% higher than 2021, and 21% higher than 2020. Europe’s plant-based sector also saw a 15% increase in venture capital deals in 2022 versus the previous year, raising €284 million ($305 million).

Home to much of the world’s scientific and commercial talent, Europe has a unique opportunity to play a leading role in plant-based and cultivated meat – and a transition to a more sustainable food system is essential to achieving the goals of the European Green Deal. But as with any emerging industry, the alternative protein sector needs to be strategic to maximise its impact.

Introducing our market research work

In order to accelerate the alternative protein market as quickly and efficiently as possible, the Good Food Institute Europe conducted a market research study to identify the most pressing challenges across the industry in Europe.

Over three months in 2021, our corporate engagement team conducted 26 interviews with experts in plant-based, cultivated and fermentation-made proteins to discuss existing challenges and future bottlenecks. Our interviews with investors, entrepreneurs, scientists, ingredient suppliers, food manufacturers and more gave us a robust understanding of the current situation across the value chain.

As a nonprofit, we value sharing knowledge freely and generating open-access information that will benefit every innovator in this space. These resources will enable you to find concrete opportunities to get involved with – and accelerate – the vital transformation of our food system. As you’ll see, there are many ways to contribute to feeding our growing population in a secure, sustainable and just way.

Key themes

In addition to the specific challenges and bottlenecks identified, a number of overarching themes were raised that impact the whole value chain.

The most frequent topic raised was Europe’s complex regulatory process. GFI Europe’s policy team is working to ensure there is a robust, fair and evidence-based path to market, so that plant-based and cultivated meat can fulfil their potential to create a more sustainable, secure and just food system.

Another common theme was the need for more productive collaboration across the value chain. While there will always be a need for some privacy to protect competitive advantage and intellectual property, alternative protein companies, suppliers, and ecosystem members can and should work together to create win-win outcomes.

Finally, as the sector grows, increasing consumers’ access to plant-based and cultivated meat, it is imperative to facilitate a just transition towards a more sustainable food system that brings existing agricultural communities along and unlocks new opportunities for them.

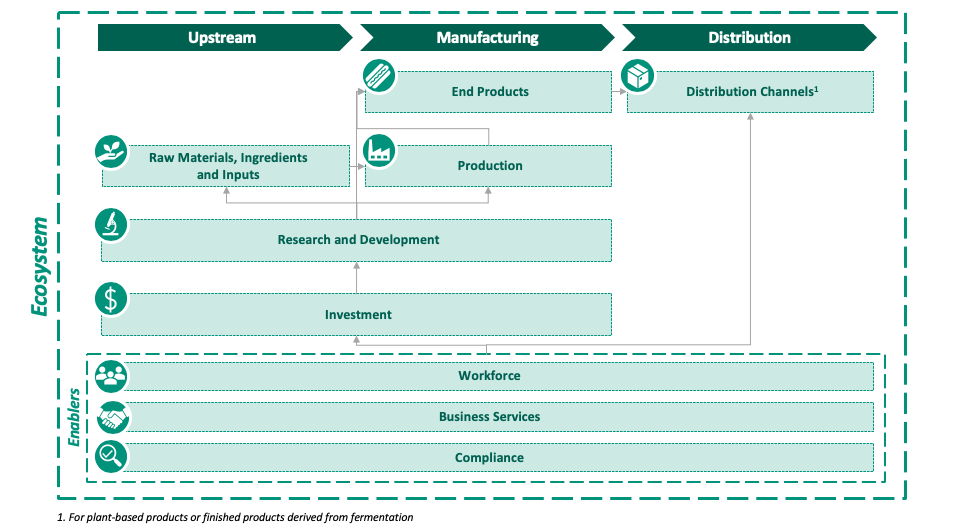

How we segment the alternative protein value chain

We map innovation priority areas and solutions to specific segments within the alternative protein value chain. Based on your background and interests, click on the segment of the value chain you are interested in learning more about and deep-dive into the key takeaways.

Innovation priorities

Investment

European companies raised €441 million in 2020 – more than four times what was raised in 2019, and 17% of the total invested in alternative proteins worldwide. Although this demonstrates promising growth, the more risk-averse culture of European investors has at times made it challenging for European startups to find funding.

As the industry continues to scale, it will become increasingly critical to generate investment from sources that have the ability to deploy significant amounts of capital midstream and upstream in the supply chain, or from sources willing to provide opportunities to utilise non-traditional financial instruments, such as venture debt.

Investment priorities

Providing infrastructure capital

As many startups begin to scale up their production, significant investment is needed to finance high capital expenditures.

While venture capital has been instrumental in accelerating the sector to date, the venture capital model is not suited to large infrastructure projects, such as building processing or manufacturing plants. Furthermore, continued venture capital investment dilutes startups.

The industry therefore needs more debt financing to fund the next stage of growth. The creation of infrastructure loan and leasing funds will help supply to keep up with demand and unlock additional economies of scale.

Driving investment into the B2B space

B2B companies in the sustainable protein sector find it more difficult to find funding as investors tend to favour consumer-facing companies. However, the success of B2B companies is crucial for accelerating innovation throughout the whole sector.

For example, companies like Motif FoodWorks, who have developed myoglobin, a heme-binding protein, will enable plant-based meat manufacturers to develop better products that replicate the flavour and aroma of conventional meat.

Research and development

Europe is home to much of the world’s scientific talent, in part due to the European Union’s focus on research and innovation through funding programmes such as Horizon Europe. Horizon Europe will provide €95.5 billion in funding between 2020 and 2027 to tackle climate change, help achieve the UN’s Sustainable Development Goals, and boost the EU’s competitiveness and growth.

While the food R&D industry has historically focused on incremental improvement, the emerging alternative protein market requires creative and groundbreaking innovation. Visit our public research funding page to learn more about how GFI Europe works to secure more government funding for plant-based and cultivated meat research.

Scientific priorities

Developing species-specific research toolkits for cultivated meat

For model species like humans and mice, a vast array of academic and commercial research tools have been developed that enable researchers to easily manipulate, characterise and screen cells, and to probe their behaviour.

For meat and seafood-relevant species, very few of these tools – such as genetic constructs, antibodies, and sequencing probes – have been developed, creating a huge barrier to entry for researchers wishing to work with cells of these species.

Coordinated efforts to develop standardised, comprehensive research toolkits of these species would exponentially accelerate cultivated meat and seafood research.

Identifying new host strains for fermentation

Identifying the best protein strain for fermentation-made products can be a time consuming and expensive process. Each strain offers its own functionality in flavour, efficiency, cost, and nutrition.

A systematic, open-access, comprehensive analysis of novel microbial strains could drastically expand the available strains that can compete on flavour, efficiency, cost, and nutrition.

Education and training

Building a skilled workforce

The plant-based, cultivated meat and fermentation industries have a significant need for workers and innovators with specialised knowledge spanning multiple traditional disciplines. However, since few universities offer alternative protein degrees or dedicated subject matter, most relevant knowledge has to be learned on the job.

The industry needs educational programming that can cover the depth and complexity of knowledge, experience and skills required within the context of traditional academic institutions as well as post-graduate professional development and training opportunities.

These programmes could also expand the R&D talent pipeline from scientific communities – cell biology, stem cell biology, biopolymers, materials science, 3D bioprinting – as well as biotech, biopharma, and established agrifood and meat companies.

Training and reskilling people to work in alternative proteins will streamline the labour transition needed to scale the industry. The need for training and education will also support the creation of new businesses and institutes, facilitating market competition and scientific collaboration that will help generate industry-advancing products, services, and ideas.

Collaboration

Catalysing academic-industry collaboration

Academic-industry collaborations are essential for advancing alternative proteins because they help build robust talent pipelines, create clear commercialisation pathways for academic research, and drive alignment on priority research questions, challenges and potential solutions.

However, challenges navigating ownership of the intellectual property generated through such partnerships has led to a lack of collaboration. To encourage greater collaboration, the sector needs to build better, standardised frameworks and platforms for coordinating connection and partnership across academic and industry stakeholders.

Fostering R&D partnerships

Collaboration within the industry among different value chain players has been challenging due to intellectual property concerns. However, with new and innovative inputs (proteins, fats, flavours, growth factors, cell media, etc) constantly entering the market, there is an opportunity for suppliers and manufacturers to work together more holistically to optimise product formulation and the compatibility of various inputs.

Knowledge sharing and collaboration like this would benefit the entire industry by reducing duplication of efforts within individual companies, pooling resources, and fuelling innovation.

Raw materials, ingredients and inputs

In Europe today, the main agricultural crops are cereals (wheat and barley) and oilseeds (rapeseed and sunflower). However, this will change over time as the amount of land dedicated to protein crops is projected to increase 37% by 2030 to meet the strong demand for more plant protein crops.

This will likely lead to larger volumes of the protein crops grown in Europe, such as field peas, broad and field beans, and lupines – which will help supply the European plant-based sector with more local and diverse proteins.

Meeting demand for alternative protein ingredients

Forecasting demand for raw materials, ingredients and inputs

Demand for raw materials, ingredients and inputs is outpacing supply, even for the most widely available plant-based proteins like soy and wheat. However, ingredient suppliers are hesitant to increase supply as it is difficult to predict what demand will look like in the short- and long-term.

Publicly available demand forecasts for novel and existing raw materials, ingredients and inputs would address these key knowledge gaps. These forecasts would be particularly valuable if segmented by product type, region, and consumer demographics. Scenario analyses, influence diagrams, and Monte Carlo calculations would enable more effective second- and nth-order estimates about what will be required from upstream suppliers in the value chain. They would also inform technical, regulatory and consumer demand milestones.

Scaling up infrastructure for local, non-GMO and novel crops, and cultivated meat inputs

As the industry continues to mature and food manufacturers and startups seek to meet evolving consumer expectations, there is increasing demand for novel, non-GMO, and local ingredients. However, it can be challenging to establish the agricultural infrastructure – from seeds and farm equipment to storage and transportation – necessary to scale novel inputs efficiently and effectively.

Additionally, in the cultivated meat industry, inputs (such as media and growth factors) are currently being used in small quantities, but there will be a significant uptick in demand for these inputs as the market scales, posing potential supply chain and cost issues.

To motivate farmers to switch to novel species or cultivars and to de-risk their first few seasons, governments should provide insurance or price guarantees, and tailored technical assistance programmes to ensure that alternative protein inputs can be a profitable and competitive option for growers.

Encouraging co-product valorization

Companies can de-risk operations by exploring either the valorization of side streams from their own processes, or sourcing these secondary materials from external suppliers.

Uses for traditional crop side streams (like husks) or processing fractions (like leftovers from protein isolate extraction) have been identified in some cases – but as demand rises for novel protein sources, finding efficient and valuable ways to commercialise all plant products and byproducts is a major opportunity.

For cultivated meat and fermentation, the challenge is finding ways to recycle or upcycle spent media – the most significant waste product in terms of volume.

Some fermentation companies are also utilising industrial food waste as an input to create a circular process, although this comes with additional regulatory implications to navigate.

Optimising ingredients

Establishing ingredient standards

Ingredients from different suppliers exhibit a range of sensory and functional characteristics, leading to undesired variability in end product formulation. Plant-based meat manufacturers would benefit from raw materials processors and farmers working in concert to develop high-quality, homogenous ingredients.

Better analytical tools for predicting plant-based ingredient performance could also improve manufacturing efficiency and create more transparent ingredient markets. Tools are needed to predict how ingredients will perform in final product applications like plant-based meat and dairy and under various processing methods. Companies could commercialise these tools themselves (in the form of assay kits or analytical equipment) or provide ingredient characterisation as a service.

Driving down costs and optimising cultivated meat inputs

Existing media and growth factor supply chains have largely been developed for the price-inelastic biotech and biopharma industries. Thus, they are too expensive, at too small a scale, and manufactured under certification regimes inappropriate for cultivated meat production.

Research on how to effectively recycle or reuse inputs, such as growth factors, at a low cost and on a larger scale, would help drive down costs.

Processing

Innovating ingredient processing

There is a need for greater exploration of processing innovations, including cheaper methods of protein extraction that can be done efficiently at smaller scales. Ingredient companies today are looking into more efficient deoiling methods, enhancing protein concentrate offerings, and more.

Beyond traditional chemical or mechanical processing methods, ingredients companies and academics should further explore enzymatic and biological processing for alternative protein purposes.

Production

The food and drink industry is Europe’s largest manufacturing sector, generating €266 billion of value-add to the economy and employing 4.82 million people in 2020.

The plant-based sector in the EU and UK is set to grow to €7.5 billion by 2025 – creating huge potential for additional jobs and economic growth. The cultivated meat sector has the potential to add 16,500 jobs and £2.1 billion to the economy by 2030 in the UK alone.

Technology

Optimising processing techniques

There is a significant opportunity to improve, optimise and innovate on current processing techniques for plant-based, cultivated and fermentation products.

Specifically for plant-based, there is an opportunity for equipment companies and researchers to optimise extrusion for plant-based production, as well as to look into novel methods for texturising and structuring plant-based proteins, such as shear cell, 3D printing, and electrospinning. These innovations will help to improve the taste and texture of end products.

Optimising the cultivated meat production process for scale

Given the nascent stage of the cultivated meat industry, no company has yet successfully scaled production to industrial levels, so there remains uncertainty around how cells will behave at scale.

In March 2021, independent researchers CE Delft released the first techno-economic assessment of cultivated meat to be based on industry data. The development of additional techno-economic models that reflect the latest data provided by companies will be essential to reflect growing expertise and experience, and to guide future process improvements.

Infrastructure

Increasing available, suitable infrastructure

Currently, there is not enough alternative protein manufacturing capacity, from pilot to demonstration to full-scale, to meet demand.

To meet market expectations for plant-based, cultivated and fermentation products, vast amounts of additional infrastructure will need to be built and existing infrastructure, such as from meat or biopharma, may have to be repurposed.

Facilitating production partnerships

Finding production partners can be a complex and time-consuming process for food startups and organisations to navigate on their own, whether they are looking for co-manufacturing space or a production partner.

Resources and services that make it easier to locate, filter and prioritise partnership efforts would make this easier for startups and add value to existing companies looking for new partners, customers and trends.

End products

With a population of over 740 million people spread across 44 countries, Europe has many different cultures, dietary habits and culinary traditions. This is a unique challenge for alternative protein companies, as they must adapt their product development and marketing to cater to regional nuances.

Product development

Perfecting taste

The success of the alternative protein industry rests upon the ability to make food with identical or superior flavours and textures to conventionally produced meat, egg and dairy products.

While we’ve seen significant improvements, few alternative protein products have achieved this to date. A recent study across the US and Europe showed that only 30% of respondents agreed that plant-based meat tasted as good or better than animal-based meat.

As taste is critical to consumer’s trial and acceptance of these products, companies must invest in additional R&D to perfect these products, and governments must fund open-access R&D.

Making alternative proteins more affordable

A recent study in the UK showed that four out of every five plant-based products cost more than their animal-based alternatives. This price difference remains a barrier for consumers to try and continue buying these offerings.

This will be especially relevant in the cultivated meat industry, where costs are currently a barrier to commercialisation – but research by CE Delft demonstrates that, with the right investment in innovation and infrastructure, cultivated meat could be cost-competitive by 2030.

Showcasing benefits

Demonstrating nutritional advantages

Demonstrating nutrition equivalence or advantage over animal counterparts will help win over European consumers. European consumers have increasingly high standards for the nutrition and clean label of these products – something companies must keep in mind as they perfect the taste and texture of plant-based and cultivated meat.

There are many approaches these companies can take, such as prioritising a clean label, sourcing local and non-GMO ingredients, and matching or exceeding the nutritional properties of conventionally produced animal products.

Introducing consumers to cultivated meat

Demonstrating sustainability advantages

It will be incumbent upon companies to demonstrate the environmental benefits of cultivated meat.

Conducting rigorous life cycle assessments will be critical. These analyses should note the potential for increased efficiencies across all stages of the plant, fermentation, and cellular agriculture life cycles, as well as the opportunities for increased efficiency that come with scaling up production.

It will be crucial to continue these sustainability studies as the industry reaches commercial scale to capture the full effect of this shift.

Educating consumers on cultivated meat

The majority of today’s consumers are unfamiliar with cultivated meat, so companies will need to educate consumers on what their products are and earn brand loyalty in creative ways.

One example is branding their products with a European country of origin, leaning into Europeans’ proud food culture around local sourcing and identity.

Distribution channels

The European continent is made up of 44 countries, each with their own language and food culture. This presents a unique challenge for alternative protein companies expanding throughout Europe, as it requires a significantly larger distribution network and the adaptation of branding and packaging strategies for each market.

Partnerships

Making connections

Distribution can often be a complex space for young brands to navigate, with a lack of publicly available knowledge about how to approach distribution strategy.

Having more informational resources and matching mechanisms to connect plant-based and cultivated meat companies with the brokers, consultants, distributors, import/export service providers, and other intermediaries would help companies to bring products to market more quickly and profitably, and increase consumer accessibility.

About the author

Carlotte Lucas leads our corporate engagement work, connecting with companies and investors across Europe to encourage investment and innovation in alternative proteins.

More industry resources

European messaging for cultivated meat

What do consumers in France, Germany, Italy and Spain think about cultivated meat – and how can we explain the…

Industry consultants

Find consultants who can offer insights to help you evaluate plant-based, fermentation and cultivated meat companies you’re considering investing in.

Seafood industry update

The plant-based and cultivated seafood industry’s commercial landscape, investment, US sales data and consumer insights from 2021.

One-page explainer on the science of sustainable protein

How to explain the science of plant-based, cultivated meat and fermentation to the public in plain, accessible language.

Plant-based state of the industry report

Plant-based in 2021: new product development, investment analytics, scientific and technical advancements, consumer insights, regulatory developments, and more.

Cultivated meat state of the industry report

Cultivated meat in 2021: the commercial landscape, investment statistics, regulatory and industry developments, scientific progress, research priorities, and more.

Fermentation state of the industry report

Fermentation in 2021: the competitive landscape, innovation opportunities, product and ingredient applications, investment trends, regulatory status, and more.

Techno-economic assessment of cultivated meat

Study of the cost of producing cultivated meat at scale, conducted by independent researchers CE Delft.